This is the third post in a four-part series on the history of Australia’s gas industry.

2015: The east coast’s liquefied gas nightmare begins

It quickly became apparent that there were a few wrinkles in the gas industry’s grand plan. Firstly, the gas companies had signed long-term contracts with customers overseas (primarily in Japan, China and South Korea) to supply them with a fixed quantity of gas at a fixed price. The problem was that many of these contracts had been signed before all the gas supply had been developed.

In some cases, companies had overestimated the size of their gas reserves. In other cases, opposition from landholders concerned that coal seam gas extraction had been poisoning the land and underground water sources meant that prospective resources could not be developed. This opposition coalesced into the Lock the Gate movement in 2010, bringing together large parts of regional Australia to oppose gas developments on farmland, particularly coal seam gas. All this meant that gas companies were having difficulty running their new expensive export facilities at 100% capacity.

But this was a small problem with an easy solution for the gas companies. Some of Australia’s gas was sold domestically on the spot market – that is, the gas is not tied to a particular customer under a long-term contract (it goes to the highest bidder). Prior to the export facilities coming online, gas was often sold in Australia for around $4/GJ. But the gas exporters could easily afford to outbid these prices – after all they could sell gas to customers in Asia for two or three times this amount.

So the gas exporters began buying up gas intended for the domestic market. Suddenly, energy-intensive manufacturers were having to match overseas prices to keep being supplied by gas. The price of gas in Australia skyrocketed. And as long-term gas supply contracts with industrial users began to expire, gas companies realised they could start demanding higher contract prices.

The vertical integration of some gas companies made these problems even worse, as many gas producers for the domestic market (eg. Santos) held part ownership of the export facilities.

So began the east coast’s gas nightmare, which has continued to this day.

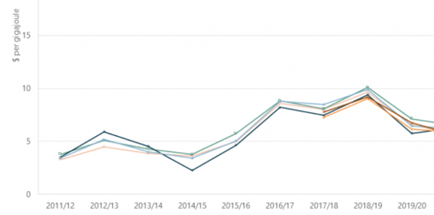

You can see the doubling in the domestic gas price in the graph below from the Australian Energy Regulator. Prices remained around $5/GJ prior to 2015, before surging upwards to $10/GJ in 2018. (Prices alleviated somewhat in 2019/20 primarily due to the pandemic but they never returned back to pre-2015 levels).

Graph 1. The average domestic gas price by state (edited). Source: AER

Each year since 2015, the same routine has played out:

Large energy users are forced to compete with gas exporters for gas supply. The gas exporters buy up so much gas that the ACCC and AEMO warn of potential gas shortages – but the gas exporters sit down with the government at the last minute and commit to keeping just enough gas onshore to prevent a shortage (but not enough to cause the price of gas to fall). And each time, the gas industry takes the credit for saving Australia from blackouts, lamenting that this could all be avoided if Australia kept opening up more and more areas for them to dig for gas.

Let’s pause for a minute to reflect. In 2000, the east coast produced 15.5bcm of gas. We consumed about 15.6bcm of gas that year – supply and demand were pretty much balanced. In 2010, 23.9bcm was produced and we used 19.7bcm – a surplus of 3.2bcm. In 2020, 57.8bcm was produced and we used 21bcm – a surplus of 36.8bcm. Australia’s demand for gas grew slowly in the first half of the 2010s, and it has actually fallen since its peak in 2017.

Australia has never produced more gas than it does now. And we are using less gas. Yet prices have never been higher. What gives? Any economist will tell you that in a functioning market supply and demand are linked: if supply is high or demand is low, prices should fall. If supply is tight or demand is high, prices should rise. Why doesn’t Australia’s gas market reflect these realities?

As many energy analysts have pointed out, calling Australia’s wholesale gas supply market a “market” is not really accurate. The gas industry isn’t made up of lots of individual players competing with each other to provide the best value product. The gas industry is a cartel, where companies work together (directly or indirectly) to create artificial scarcity to keep prices high. It is market in name only, where gas companies say “we will sell you gas for this price, and if you don’t agree we won’t sell you gas, and you won’t be able to get gas from anywhere else, so you’ll have to shut down”.

It has been noted by the ACCC “that almost 90 per cent of the proven and probable (2P) [gas] reserves in the east coast in 2021” were controlled by liquefied gas exporters, either directly or indirectly.

But what can be done about a powerful cartel controlling an essential resource and extorting Australian businesses? The Federal Government can intervene of course. But Australia’s free market-inclined Coalition and Labor Governments do not like the idea of interfering with one of Australia’s most powerful cartels. And honestly, they are probably scared of them too. Governments of any stripe will not intervene unless the gas cartel does something so wildly irresponsible that they are left with no choice. And the gas industry is smart enough to avoid that.

Or so we thought, until 2022 happened.

One reply on “How to lose friends and alienate people (or, A very short history of the Australian gas industry): Part 3”

Oh you leaving us in suspense….. 🙂

>

LikeLike