This is the final post in a four-part series on the history of Australia’s gas industry.

2022: The gas industry spits in Australia’s face

In the period from 2015 to 2022, the gas industry cartel more or less did what it wanted, partly thanks to a complaisant Federal Government, partly due to an excellent campaign of obfuscation and blame-shifting lead by lobby group APPEA and the rest of the gas industry.

But as with any organisation or individual that has gotten away with doing whatever it wants for a long time, hubris and entitlement eventually creep in.

In February 2022, Russia invaded Ukraine. Europe substantially cut piped gas imports from Russia, which had been one of the world’s largest gas producers. Now much of Europe was trying to import liquefied gas to fill some of the gap to avoid energy shortages.

This was a bonanza for liquefied gas exporters. Liquefied gas prices had already been rising in late 2021 due to supply chain constraints as global demand recovered from covid lockdowns. But with a surge in liquefied gas demand in Europe, things got totally out of control.

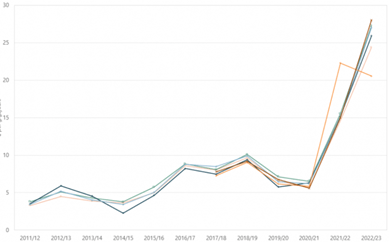

Remember that graph of domestic gas prices from Part 3? Well, I actually chopped off the end of the graph. This is what the complete graph looks like:

Graph 1. The domestic gas price by state (complete). Source: AER

The increase in gas prices in 2022 is truly astronomical and without precedent.

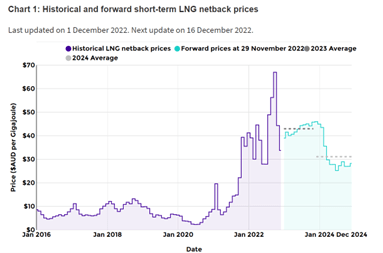

The graph below is from the ACCC and shows the liquefied gas netback price – effectively the price a gas exporter can expect to receive for selling their gas overseas.

Graph 2. The price of liquefied gas by month. Source: ACCC

In 2016 and 2017 it averaged $5-10/GJ. Between January 2016 and September 2021, it had only risen above $15/GJ once. Then things went crazy. In October this year, the price peaked at an eye-watering $67/GJ. Now it is $34/GJ, still three to four times higher than it was in mid-2021.

It doesn’t need to be this way. Over in Western Australia, the average price of gas from July-September was just $6/GJ. In large part thanks to their long-standing domestic gas reservation policy, Western Australians are paying as much as 91% less for their gas than those of us on the east coast.

Let’s be clear about what the impacts of sustained extreme gas prices are: manufacturers and other large energy users will go bankrupt and household energy bills will skyrocket. These high gas prices are also driving up the cost of electricity (for complex reasons which I won’t go into here), driving up inflation, which in turn is driving up interest rates. This is a national crisis. And it had to be brought under control.

But the gas industry seems oblivious, or perhaps indifferent, to the real world suffering caused by their war profiteering. The cost of producing gas has not changed over the last year – gas companies were already making very healthy profits. One study has estimated that gas production on the east coast is still profitable at $7/GJ. But if you can price gouge, why not? The gas cartel had been doing what it wanted for years and when the liquefied gas price went bonkers, I doubt they even contemplated the possibility that the government might step in to stop them.

Perhaps under the previous government they would have been right not to be concerned. But the new Labor Government – which to be clear, has been friendly with the gas industry for a long time – clearly felt like it had no choice but to act.

This week, the government introduced a temporary price cap of $12/GJ and a mandatory “reasonable price” provision in gas contracts.

The gas cartel was indignant and furious. First Shell and now Woodside, cheered on by parasitic investment banks like Credit Suisse, have threatened to withhold gas supply and create an artificial gas shortage for Australian households and businesses if this law is passed. Interestingly, they seem far angrier about the “reasonable price” provisions than the price cap – the price cap is temporary after all and at $12/GJ, gas companies will still be making large profits. But a reasonable pricing provision, depending on how it is applied, could permanently limit their ability to price gouge Australian businesses and constrain their ability to artificially limit gas supply.

At the time of writing, the Federal Government’s legislation has just sailed through the Parliament, just 6 days after it was first announced.

Conclusion: Will the gas industry finally get what it deserves?

So where does this sorry history leave us? A broken energy pricing system, an angry, rich and powerful cartel, an emboldened Federal Government, and ropeable businesses and households. A volatile mix for sure – but will it change anything?

Has the gas industry’s period of unchecked power come to an end? Can the government harness near-universal community anger to enforce a permanent price cap, a gas reservation policy or a super profits tax? Certainly Industry Minister Ed Husic seems up for the fight. Or will the gas industry regroup and come to an accommodation with the government that keeps their power largely intact? Only time will tell.

But there is one thing we do know: this crisis has made it abundantly clear from Europe to China, India to Japan that gas is unaffordable. The argument that gas can be a “transition fuel” to renewables is dead. The gas industry may keep getting very rich for a few more years but their obsession with super-profits is speeding up demand destruction. Maybe one day we will look back on 2022 as the beginning of the end of gas.

Much of the information in this series of posts I have learnt over several years working within and adjacent to the energy sector. I have only included references for controversial or more recent events.

Data on gas production and consumption was sourced from the Australian Government’s Australian Energy Statistics, particularly Tables N and Q. Data on mains gas connections was sourced from the Australian Bureau of Statistics (unfortunately this eight year old dataset is the most recent source available on this subject).

One reply on “How to lose friends and alienate people (or, A very short history of the Australian gas industry): Part 4”

I loved reading this Louis – well done!!!

>

LikeLike